Real Estate Tokenization

Discover how DigiShares empowers property owners and investors through secure, blockchain-based real estate tokenization. From fractional ownership to automated investor management, unlock the future of real estate investment.

“Our clients tokenize their real estate for three reasons: digitization and automation of processes, fractionalization to reach new types of investors, and the massively increased liquidity.”

Claus Skaaning

CEO DigiShares

Why Choose DigiShares?

Launch your own real estate crowdfunding platform

Offers instant liquidity through our OTC marketplace

Full shareholder functionality: shareholder meetings, votes, etc.

Secure Electronic Signatures

Support for most global currencies

Token Compatibility with Custodians & Exchanges

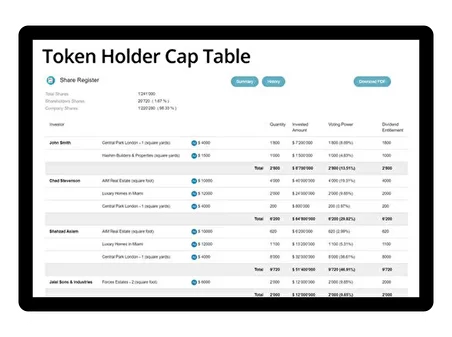

Advanced cap table management

Uses audited smart contracts for high safety and security

Benefits of Real Estate Tokenization

- Launch your own real estate crowdfunding platform

- Automate investor management and document handling

- Access global real estate fundraising opportunities

- Raise capital more efficiently with programmable shares

- Ensure compliance through secure smart contracts

- Electronic signatures

- Tokens are compatible with exchanges, custodians, etc.

- Enjoy fractional property ownership with lower entry points

- Trade digital shares on 24/7 markets

- Diversify investments globally with transparency

- Benefit from rapid settlements and increased liquidity

- Explore blockchain real estate investment options

- Customize your tokenization platform quickly

- Scale with recurring revenue from multiple assets

- Become a regional tokenization provider

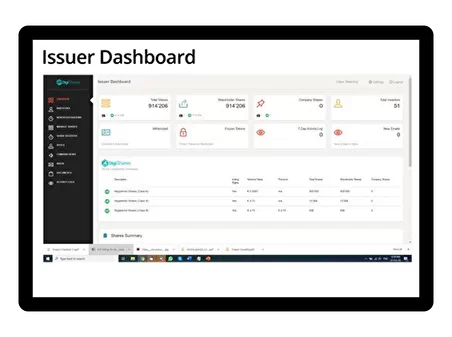

How DigiShares Helps

DigiShares offers an end-to-end real estate tokenization platform that supports every phase of your investment lifecycle.

- Investor onboarding with KYC/AML compliance

- Token purchase and secure digital transactions

- Electronic signatures and smart contract execution

- Tokenized shareholder registry across multiple classes

- Real-time investor communication and voting tools

- Dividend distribution and automated reporting

- Token freeze and reissuance management

- Internal secondary market for peer-to-peer trades

- Integration with custodians, banks, and payment systems

- Compatibility with third-party exchanges and wallets

Explore how real world asset tokenization works and unlock new investment channels.

Compliance and Regulations

DigiShares uses audited smart contracts and offers full compliance support. Our platform handles:

- Global KYC/AML standards

- Cross-border transaction restrictions

- Lock-up periods, dividend automation, and more

DigiShares uses audited smart contracts and offers full compliance support. Our platform handles:

What is Real Estate Tokenization?

Tokenizing real estate assets brings transparency, liquidity, and automation to traditionally illiquid markets. Whether you are a developer, fund manager, or property owner, blockchain-based property investments are the key to democratized real estate ownership.

Value Proposition for Tokenizing Real Estate

Tokenizing your real estate project can help you raise capital more efficiently by giving investors unprecedented access to private real estate investments, transparency, and liquidity.

Pains

- No more costly, paper-based workflows

- Increased liquidity and accessibility, almost zero liquidity

Primary Gains

- Digitized and automated processes

- Immediate trading and liquidity (premium: 20-30%)

Secondary Gains

-

Ability to fractionalize/democratize

- reduced ticket size

- increased diversification - Access to new types of investors

- Access to new global infrastructure of investors and secondary liquidity

- Programmable tokenized shares for automation of cross-border transfers, lock-up periods, dividend payment, etc.

- Smart “functions”: custody, DeFi lending, atomic transfer, etc.

- Increased security by removal of human errors

- Transparency and traceability

Start Tokenizing Your Today

Join hundreds of asset owners using DigiShares to digitize their portfolios. Whether you’re an individual or institutional investor, we help you bridge traditional real estate and blockchain technology.

DigiShares Platform

Issuance

- Investor registration and verification (KYC / AML)

- Token Purchase

- Electronic document workflow and signatures

Corporate Management

- Tokenized shareholder register over multiple share classes

- Investor communication & voting

- Dividends

- Freeze / renewal of tokens

Trading

- Internal exchange

- Integration to custodians, banks and payment platforms

Example of our works

Contact Us To Learn More About Real Estate Tokenization

Please prove you are human by selecting the: